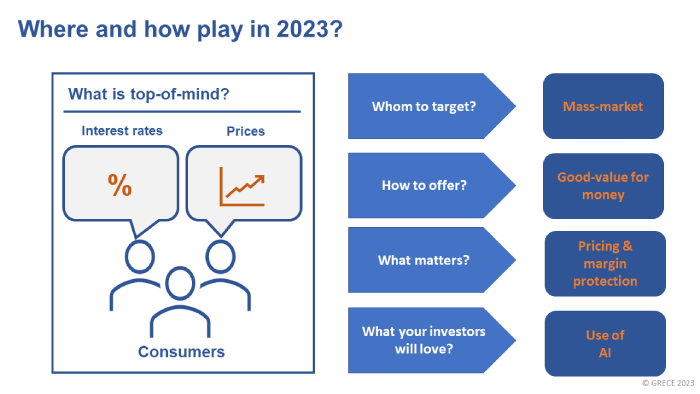

Inflation will continue top-of-mind and good-value offers will resonate with consumers. Government support will soften the impact of inflation on lower income quartiles and mass-market focused industries will do well (e.g., package holidays, fast food, discount stores).

Key trends

Higher interest rates on mortgages will hit the (upper) middle class and industries driven by this segment will face challenges (e.g., branded durables, cars). Also watch out for disruptions in the real estate sector and associated industries. For businesses margin protection will be critical as (cost) inflation will eat into margins. The hype around ChatGPT is making AI the “mainstream tech theme” of 2023.

Every year was dominated by one top-of-mind topic: COVID in 2020/21, followed by the war in Ukraine and the associated energy crunch in 2022.

This caused politics and businesses to react while some industries – for good or bad – came into the limelight. Businesses tend to react more swiftly, while politics seems slower and reacts only towards the end of the cycle. This tends to reinforce issues which are already in the making.

For instance, the Covid pandemic was petering out in 2021, but cheap money and public stimuli packages were still flowing, preparing the ground for today’s inflation.

If this is a harbinger for 2023 – with inflation being top-of-mind – then price controls and subsidies might fuel future issues. For sure it is too early to judge, though we might see distorted investment decisions and higher interest rates for longer.

Price caps will lead to underinvestment, while subsidies will lead to overconsumption and overinvestment. This will particularly affect the real estate and energy sector, but in opposing directions.

State of real estate

Real estate had a fantastic run in most of the developed world over the last decade but is now being hit by rising interest rates. This is hitting the yield of buy-to-let owners and investment firms. On top some countries are considering rent caps and “price brakes”. This puts further pressure on these investors, thus curbing investment in real estate and driving funds towards complementary income investments (e.g., bonds). This might lay the foundation for the next real estate boom in 3-5 years’ time when pent-up demand needs to be fulfilled.

Growing demand for alternatives

The contrary effect is true for the energy sector. No doubt that the development of alternative energy sources is absolutely necessary for the good of the planet, but we might see a lot of supply hitting the market over the next few years. Imagine some normalization of traditional energy flows – e.g., in case of a ceasefire in Ukraine – and we might face price gyrations similar to those in 2009 or 2020.

Furthermore, these subsidies are working against the tightening of the monetary policy. The latter aims to reduce demand while subsidies do exactly the opposite: leading to higher consumption. The widespread subsidies in the developed world can thus only mean higher interest rates for longer.

Even though finances of both businesses and households are constrained by rising rates not all sectors and segments are affected equally.

Capital intensive industries

On the business side, capital intensive industries, such as manufacturing and real estate are affected most, plus banks that extend credit to those industries and households (mortgages). By contrast, services (e.g., restaurants, personal services) continue to do well as they enjoy pent-up demand from COVID-times while they are capital light and not severely affected by rising rates.

On the consumer side, households with mortgages will be hit the most while renters might even benefit from rent caps discussed in many countries. This increases the financial pressure on the (upper) middle class while lower stratospheres will not be hit that hard. This is bad news for industries which live from the (upper) middle class: e.g., high-end travel, branded fashion, (branded) durables, and cars.

Mass market demand continues

By contrast, industries focused on the mass-market shall do better since the income of the lower stratosphere is protected and the middle class will search for cheaper options. We might see a bonanza in “good-value industries” – discount stores, package holidays, fast food, good-value fashion etc.

Within businesses the focus will shift – from supply chain issues – towards margin protection: coping with cost inflation while increasing prices or adjusting products (“shrinkflation”). At the same time capital will be allocated more carefully which does not spell good times for capital expenditure and capital goods. The time of cheap money is over.

Thus, the finance function will have a strong hand in 2023 and, if you have the luxury to pick, the finance function seems a good spot for your career in 2023.

On the tech front the collapse of FTX has finally ended the (mass) euphoria around crypto, making it more of a niche topic for aficionados going forward. The hype around ChatGPT is making AI the mainstream tech theme of 2023.

With every student using ChatGPT for writing his/her homework, investors will also expect your business to use AI to make your customer service better or streamline operations. Do not forget to include an AI page in your pitch deck!

What does this mean for starting, developing, or building a business?

All those trends have implications for building businesses, such as: What are attractive target groups? What is a good value proposition? How to pitch ideas to investors? What industries to avoid?

I expect the main implications to be:

- Mass-market services (e.g., food delivery, package holidays) will do ok as the lower (middle) class will be hit less by rising rates and might benefit most from subsidies;

- Good-value offers resonate with inflation-worried consumers: business models which offer customers a better-value alternative to traditional sources will lure consumers;

- Money will be tight in the (upper) middle class and B2C-businesses catering to this segment will have a harder time (e.g., branded durables, cars, high-end travel);

- Real estate and associated industries will be a difficult spot in 2023 but prepare for a rebound in the years to come. 2023 will not be good year for launching a Proptech business or Fintech focused on mortgages (unless it benefits from harder times in the real estate sector);

- Finance will have the say in the corporate world with a focus on margins, pricing and cost containment … if you have the luxury to pick, this seems a good spot for your career in 2023;

- The hype around ChatGPT is making AI the new ‘mainstream tech theme’ of 2023 … do not forget it in your investor pitch!